Holding Cash in a World of Zero to Negative Interest Rates

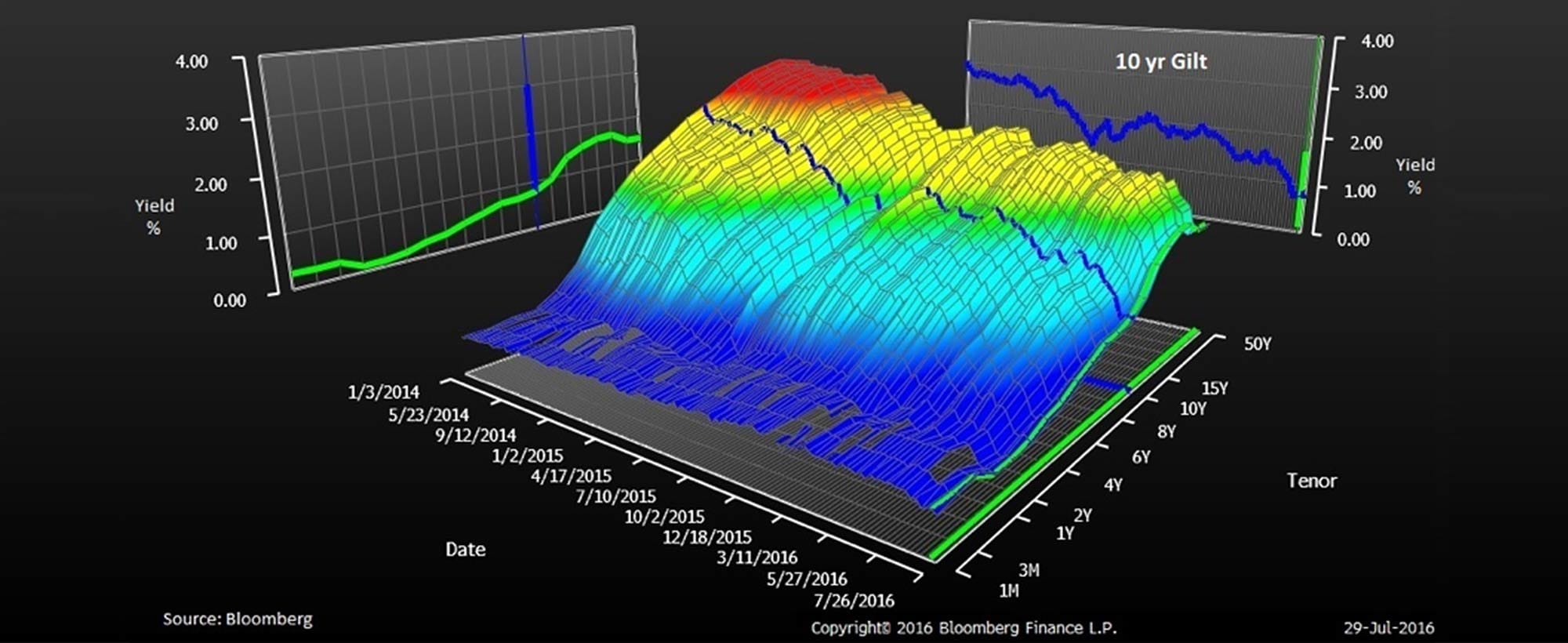

The chart below shows the rates of interest the UK government has to pay to borrow money at various maturities between 1 month and 50 years. It also shows how this has changed over time from the beginning of 2014 when, whilst the Bank of England base rate was the same as it is today at 0.5%, the 10-year Gilt yield was 3% compared to sub 0.75% today. We can see just how far rates have fallen and that the market does not expect them to rise substantially any time in the near future.

The Changing Shape of the UK Government Yield Curve from Jan 14 to Jul 2016

So what can clients do in the face of falling cash rates? It is important to have a good idea of what clients are trying to achieve with their money. Secondly, they can then consider the appropriate amount of cash they should hold. We often hold too much cash as it is somewhat of a default option, and a desire to avoid the wrong decision can lead to making no decisions at all. The right level of cash for each person will be driven by a combination of his needs and his level of comfort with investing his savings. We all have a figure for how much cash we need to hold to feel comfortable that unforeseen events can be dealt with. Once we know what that right level of cash is, we can consider how best to invest the remaining money to achieve our goals.

Having spent the time considering what you need to hold in cash and knowing you have this set aside should give you the comfort to invest a portion of your assets for the longer term. Whilst this may involve taking some investment risk it can help to reduce the risk of not achieving your investment goals.

If you would like help to review what the right level of cash is for you and how your assets could be invested to help you achieve your goals get in touch with one of our advisors by emailing advice@netwealth.com.

As always, please remember your capital is at risk and the value of your investments might go down as well as up and you may not get back the amount invested.

Subscribe to our newsletter

Share this