How to Make the Most of Available Tax Wrappers

When investing there are several factors that are out of your control, such as market performance, volatility and inflation. Yet one thing that you can influence – that significantly impacts your wealth – is the use of tax wrappers that contain your investments, and ensuring that tax-free allowances and exemptions are also used.

There are two main types of tax-incentivised wrappers for investments in the UK: pensions and ISAs. Both wrappers benefit from tax-free investment returns but pensions offer two key further advantages.

The advantages of pensions

Firstly, money paid into a pension benefits from tax relief at your marginal rate, which can mean that paying £20,000 into a pension costs you as little as £8,000.1 25% of the total pension can then normally be taken tax-free when you retire. Secondly, pensions do not form part of your estate for the purposes of inheritance tax, which can provide an additional benefit to the beneficiaries of your estate.

Changes to pension legislation, such as the reduction of the lifetime allowance to £1.03m and the introduction of the tapered pension annual allowance for those earning more than £150,0002, have not only earned HMRC an additional c£250m this year3, but also mean that it is sensible in many cases for clients to look to other tax-efficient wrappers to bolster their savings for retirement (or any other financial goal they have).

That said, even high earners impacted by the tapered annual allowance can contribute up to £10,000 per annum (gross of tax relief) to a pension, while maintaining the tax advantages discussed above. It is also possible for one spouse to provide cash that allows the other spouse to make a pension contribution (or indeed to fund a child’s pension contribution4).

Why ISAs are such a solid choice for investors

Individual Savings Accounts (ISAs) have become a slightly more attractive investment vehicle in recent years as the inheritability, flexibility and amount you can invest have all improved. They are therefore suitable for many types of clients, although the tax shelter ISAs provide is still limited to £20,000 per annum per person.

Unlike pensions, investors do not receive tax relief on contributions into an ISA, but they do benefit from tax-free growth and income, and withdrawals are tax free rather than being treated as income as they are with pensions.

Further benefits for clients who need extra

It may be that the annual level of savings you can make is covered solely by pensions and ISAs, although for many clients, something beyond this limit is also required. The solution is often to invest through a General Investment Account (GIA) that can replicate the same investment strategy that is present in a pension and ISA portfolio.

Investing through a GIA is not as advantageous as investing via an ISA or pension, but using a GIA does allow you to take advantage of your annual capital gains tax exemption (£11,700 currently), your annual dividend allowances (£2,000 currently), and your annual Savings Interest allowance (up to £1,000 currently).

Between a married couple, for example, these allowances can still add up to a reasonable degree of income or capital gains before tax is due – especially if managed in conjunction with an ISA or pension portfolio.

Two different routes with very different outcomes

The following case study shows how an investor could use their various tax wrappers, and the allowances within, to invest a total of £936,000 over 45 years.

| |

Case Study Key Facts |

| Client Age |

50 |

| Netwealth Risk Level |

5 |

| Contributions |

£600 per month for 5 years |

| Retirement Age |

60 |

| Income in Retirement |

£4,000 (net) per month |

| Inflation Assumption |

2% per annum |

| Timeframe |

45 years (to age 95) |

| |

|

| |

|

| Pension Starting Value |

|

| Pension Contributions |

|

| GIA Starting Value |

|

| GIA Contributions |

|

| Annual ISA Funding from GIA |

|

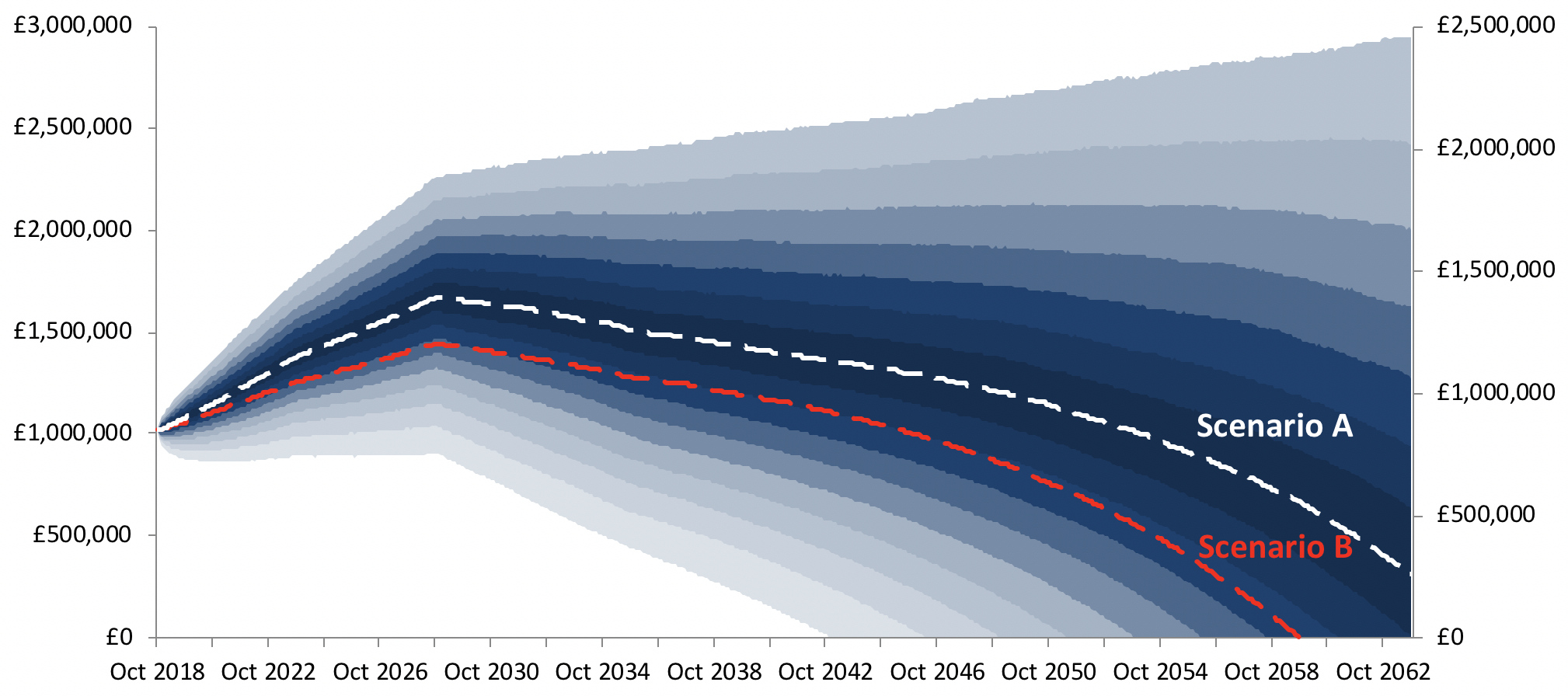

The projection below shows a range of outcomes for Scenario A whereby the investor appropriately uses the various tax wrappers available and is also carefully drawing upon those tax wrappers in retirement to fund their income of £4,000 per month increasing in line with inflation.

The white dashed line shows the average projected outcome for Scenario A which is in the middle of the range of possible outcomes (the blue areas). As we can see in the average scenario, the portfolio is able to sustain the level of drawing required, beyond age 95.

Overlaid on the same projection, the red dashed line shows the average projected return for Scenario B. In Scenario B, the investor does not make any contributions to a pension or an ISA and instead solely contributes to their GIA. In this scenario the investor is projected to run out of money at age 90 in the average outcome.

Source: Netwealth

Projected returns are illustrative and are not guaranteed.

In both cases, the gross investment return and sums invested are exactly the same, but simply by using tax wrappers appropriately the investor can benefit from at least five additional years of retirement income, which equates to £240,000 in today’s money, in this case.

Conclusion

In summary, although there are many factors to consider when investing that are out of your control, they should still be frequently assessed and taken into account so that action can be taken where necessary.

Making use of the appropriate tax wrappers (along with minimising fees, ensuring you stay invested and that you are well diversified) is very much within your control and can have a huge impact on your net returns over the long term. To focus on this is time well spent.

| |

Annual Allowance |

Tax Advantages |

Access |

| Pension |

100% of salary up to a maximum of £40,000 (lower for those earning over £150,000 p.a.) |

Money paid in net of income tax and investment returns are tax-free |

From age 55, 25% tax-free and remainder taxed as income |

| ISA |

£20,000 |

Investment returns are tax-free |

Anytime tax-free |

| GIA |

Unlimited |

Capital Gains Tax Exemption of £11,700 per annum, Dividend Allowance of £2,000, and Savings (interest) Allowance of up to £1,000 p.a. |

Anytime tax-free |

Please remember that when investing your capital is at risk.

1 If you are earning £120,000 per annum, this would be the cost. In other cases, the proportion of tax relief available would be less.

2 UK taxpayers can receive tax relief on pension contributions of up to 100% of their earnings or a £40,000 annual allowance, whichever is lower. Those with earnings over £150,000 have a reduced allowance.

3 FT article: “High earners caught out by clampdown on pensions tax relief” - 28 September 2018.

4 Non-taxpayers can still receive tax relief on pension contributions up to £3,600 (gross of tax relief).

Subscribe to our newsletter