How to Make the Most of Available Tax Wrappers

This content was last updated in July 2025 to reflect the latest UK tax allowances and investment rules

Table of contents

When investing, there are many factors outside of your control – such as market performance, inflation, or interest rates. However, one area you can control, which has a significant impact on long-term outcomes, is how effectively you use tax wrappers and allowances. Making full use of pensions, ISAs, and other tax-efficient vehicles can improve returns and reduce unnecessary tax liabilities.

Key Takeaways

- Tax wrappers like pensions and ISAs can significantly improve net investment outcomes.

- Case study shows tax allowances can extend retirement income by five years.

- Contributing to a pension attracts tax relief and shields investment growth from income and capital gains tax.

- GIAs offer flexibility but come with limited allowances and potential tax liabilities.

- Using ISAs alongside pensions can recycle capital into a tax-free environment over time.

What is a tax wrapper?

A tax wrapper is a legal structure that holds your investments and determines how they are taxed. Common UK tax wrappers include pensions, ISAs, and General Investment Accounts (GIAs). The wrapper affects whether you receive tax relief on contributions, pay tax on growth or income, and how withdrawals are treated.

There are two main types of tax-incentivised wrappers for investments in the UK: pensions and ISAs. Both wrappers benefit from tax-free investment returns but pensions offer two key further advantages.

How do pensions, ISAs and GIAs compare?

Use the table below to see how each tax wrapper differs in terms of limits, tax benefits and access.

| Annual Allowance | Tax Advantages | Access | |

|---|---|---|---|

| Pension | Up to £60,000 gross (tapered to £10,000 for high earners) | Tax relief on contributions, growth free of UK income and capital gains tax | From age 55 (rising to 57 in 2028). 25% tax-free, remainder taxed as income |

| ISA | £20,000 | All growth, income, and withdrawals are tax-free | Access anytime, tax-free |

| GIA | Unlimited | CGT exemption: £3,000. Dividend allowance: £500. Savings allowance: up to £1,000 | Access anytime. Gains and income may be taxable |

The advantages of pensions

Pensions remain one of the most tax-efficient ways to invest for retirement. Contributions benefit from tax relief at your marginal rate, so for a higher-rate taxpayer, paying £20,000 into a pension could effectively cost just £12,000. Once you reach the minimum access age (currently 55, rising to 57 in 2028), up to 25% of your pension can usually be taken tax free. The remaining balance is taxed as income when drawn.

Another advantage is that pensions do not normally form part of your estate for inheritance tax purposes, which can provide additional benefits for beneficiaries.

Recent changes to pension legislation have made them more accessible. The Lifetime Allowance was abolished in April 2024, and the Annual Allowance increased to £60,000. However, the Tapered Annual Allowance still applies to high earners. If your adjusted income exceeds £260,000, your allowance may reduce as low as £10,000. Despite this, high earners can still benefit from tax relief on contributions up to that reduced limit.

It is also possible for one spouse to fund pension contributions for another – including for non-earning partners or children – using personal allowances. Non-taxpayers can receive basic-rate tax relief on contributions up to £3,600 gross per year (£2,880 net).

Why ISAs are a solid choice for investors

Individual Savings Accounts (ISAs) remain a core part of many investment strategies. Each individual can contribute up to £20,000 per tax year, with all investment growth, interest, and withdrawals completely tax free.

Unlike pensions, ISAs do not provide tax relief on contributions, and they do form part of your estate for inheritance tax. However, their flexibility and tax treatment make them suitable for a range of goals. Withdrawals are not taxed as income, making ISAs especially useful for supplementing retirement income or funding ad hoc expenses tax efficiently.

Further benefits for clients who need extra

If your full annual ISA and pension allowances are already used, the next step for many investors is a General Investment Account (GIA). While GIAs do not offer upfront tax advantages, they can still be used tax efficiently when managed alongside available allowances.

In 2025/26, you can benefit from:

-

Capital Gains Tax exemption of £3,000

-

Dividend Allowance of £500

-

Personal Savings Allowance of up to £1,000 (for basic-rate taxpayers) or £500 (for higher-rate taxpayers)

When managed carefully – especially between spouses – these allowances can still shelter a meaningful portion of returns from tax. GIAs can also be used to fund ISAs each year, recycling capital into tax-free wrappers over time.

Case study: Same investment, different outcome

The following case study illustrates how an investor can utilise their various tax wrappers and allowances to invest a total of £936,000 over 45 years.

| Case Study Key Facts | |

|---|---|

| Client Age | 50 |

| Netwealth Risk Level | 5 |

| Contributions | £600 per month for 5 years |

| Retirement Age | 60 |

| Income in Retirement | £4,000 (net) per month |

| Inflation Assumption | 2% per annum |

| Timeframe | 45 years (to age 95) |

| Scenario B | Scenario A | |

|---|---|---|

| Pension Starting Value | £0 | £400,000 |

| Pension Contributions | – | ✔ (£600 p/m net) |

| GIA Starting Value | £900,000 | £500,000 |

| GIA Contributions | ✔ (£600 p/m net) | – |

| Annual ISA Funding from GIA | – | ✔ |

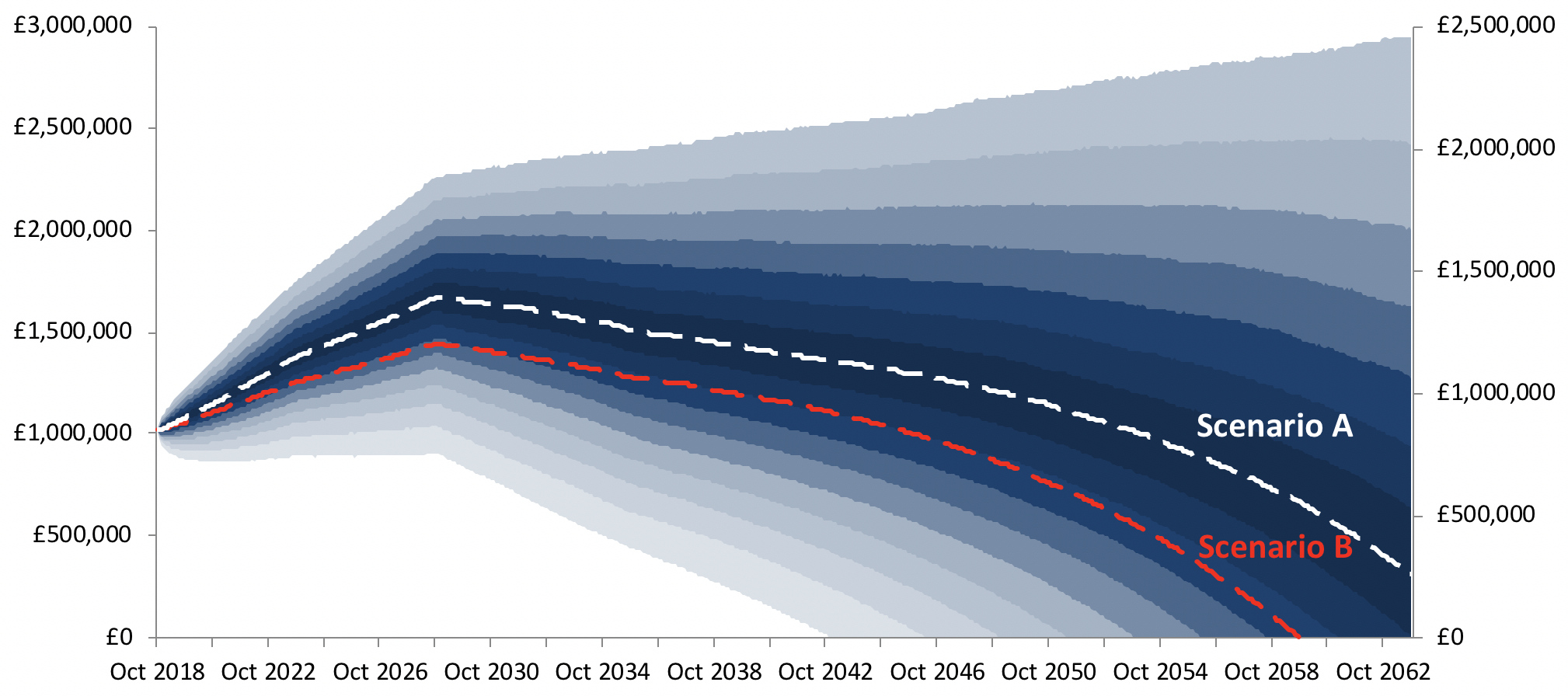

Interpreting the projection

The projection below shows a range of outcomes for Scenario A, where the investor uses tax wrappers effectively and draws on them strategically in retirement to generate an inflation-linked income of £4,000 per month.

Source: Netwealth

Projected returns are illustrative and are not guaranteed.

The white dashed line shows the average projection for Scenario A, sitting in the middle of a range of outcomes (blue shaded area). As shown, the portfolio supports the income need well beyond age 95.

In contrast, the red dashed line shows the average projection for Scenario B. In this version, the investor uses only a GIA and does not contribute to a pension or ISA. Here, the portfolio is projected to be depleted by age 90.

Key insight

In both cases, the gross return and total amount invested are identical. Yet by using tax wrappers strategically, the investor in Scenario A achieves five more years of sustainable income – worth approximately £240,000 in today’s terms.

Conclusion

In summary, although there are many factors to consider when investing that are out of your control, they should still be frequently assessed and taken into account so that action can be taken where necessary.

Making use of the appropriate tax wrappers (along with minimising fees, ensuring you stay invested and that you are well diversified) is very much within your control and can have a huge impact on your net returns over the long term. To focus on this is time well spent.

Further Resources

Investing with Netwealth: Smarter, simpler, lower cost

Netwealth offers low-cost, diversified portfolios with expert management and intuitive digital tools. See how efficient investing can help you achieve better long-term outcomes.

Contact our team today and take control of your financial future.

More from Netwealth