What's Behind the Weakness in UK Assets?

Rarely do events in financial markets lead the main evening news. This highlights the magnitude of UK bond market volatility and sterling’s fall in the past few days, and underscores how important it is for investors to be aware of the consequences and to be prepared.

Why has sterling fallen?

Some of the moves from sterling were reinforcing trends that were already in place, with the US dollar getting stronger this year against most other currencies. The US dollar is often viewed as a safe-haven currency and with so much uncertainty in the world – from the war in Ukraine to soaring energy costs – investors globally have increasingly favoured its implicit security in 2022.

You could argue that the Bank of England was too slow to recognise the inflationary pressures that were building up due to the different events this year. It put interest rates up from 1.75% to 2.25% last week and is clearly biased to do a lot more. The challenge is the dynamics of this inflation picture are changing quite quickly.

Yet the Chancellor last week also gave markets more reasons to be negative on sterling. While there was much emphasis in the mini-Budget on cutting taxes there weren’t any clear revenue increasing measures. How are the proposals outlined to be paid for? This has put immense pressure on borrowing costs, with the debt management office having to outline plans to sell an additional £72 billion of gilts (government bonds) as a result.

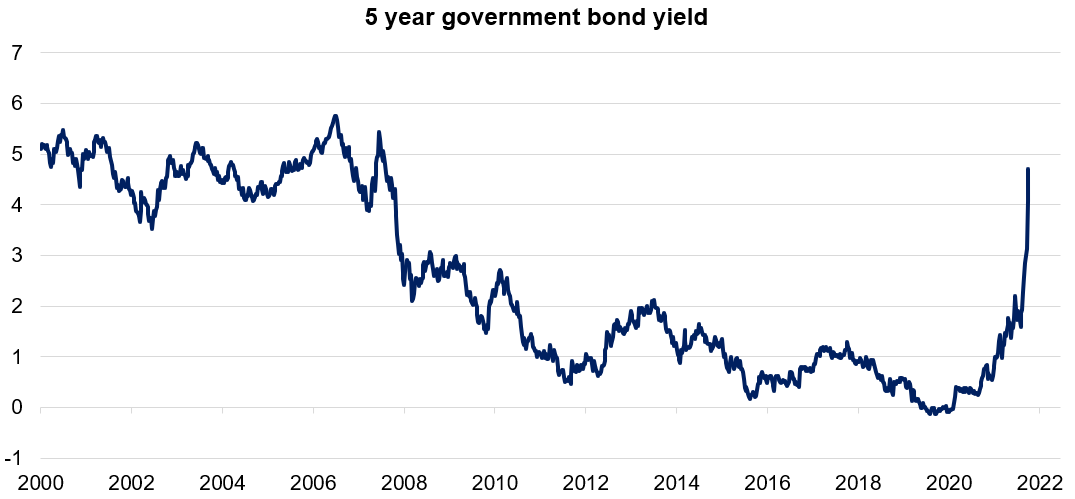

While the crisis for many observers will be viewed as the optics around sterling, the real danger is the lack of confidence in UK gilts – demonstrated by the sharpest surge in decades in gilt yields (shown below) over the past few days, pushing prices lower.

Source: Bloomberg

In short, international investors have lost a great deal of conviction in the government’s ability to be effective stewards of the UK’s finances, and in sterling, too.

What does this mean?

As so many goods in the UK are imported, most consumers and businesses directly face higher costs. With government change on tax rates perceived as inflationary, the cost of borrowing across the board will also likely increase – with mortgage rates and other loans all set to go up.

Investors in UK government bonds are calling for a more credible fiscal plan to be put in place by the Chancellor to stabilise rates in a key asset market – the perception of greater riskiness is putting the stability of all assets at risk.

The further risk now is that the international currency market has got the bit between its teeth – they don’t always focus purely on fundamentals. Many people trade just on momentum and so the downward pressure is there, and likely to persist until the government and/or the Bank of England act to reassure investors.

For many UK market participants, that reassurance can’t come soon enough.

How is Netwealth positioned to respond?

The key to creating successful investment portfolios is to make sure they are suitably diversified – by asset class (stocks, bonds, cash, commodities etc) and by location. We always try to ensure we are appropriately globally diversified and closely monitor national and global events so we can respond if need be.

Right now, markets and investors around the world are attempting to adapt to the likelihood that interest rates will face more upward pressure. We’ve long been used to an environment where interest rates have stayed very low due to subdued inflation, so even though growth has been modest in many countries, at least investors knew where they stood with regards to interest rates.

Central banks now faced with inflationary pressures are pushing the cost of money higher and as these liquidity conditions tighten further globally, it makes a much tougher environment for many different investments. In particular, shares in companies where corporate profits will be more under pressure look pretty challenging.

We have higher levels of cash in portfolios than usual, we are holding more in US dollar assets than usual and we’re also avoiding the bonds of companies with weak balance sheets for now. We’ve had less exposure to European and UK assets for much of this year, on the basis that the fundamentals in the US look a little stronger.

On a positive note, the result of all this volatility is that valuations of different assets are getting cheaper, so we’re staying alert and making sure we keep investment costs down. As ever, we’re keeping portfolios diversified to manage our way through the current uncertainty.

What should investors do now?

While any disruption in financial markets is troubling, the most prudent approach – at least until there is more clarity around current events – is to remain invested. Trying to time or second guess the market, or actively pick enduring winners is very difficult.

Markets have been volatile throughout this year, but an experienced team by your side can help – by keeping cool and responding effectively to changing market conditions. If you would like to know more, please get in touch.

Please note, the value of your investments can go down as well as up.