One needs to examine the details of these to ensure that they are as comprehensive as they should be. Lest we forget, the Treasury Select Committee highlighted large groups were excluded from help previously. But there was a boldness to yesterday’s announcement that goes someway to answer those who wanted the Furlough Scheme extended.

The Chancellor addressed the immediate need to bridge the gap between the ending of existing support and the hoped for return to normal of the economy next spring. But, both yesterday and in cancelling the Budget, he has avoided addressing the issue of affordability.

Understandably, there is always going to be an element of catch-up in much of the policy stance during a pandemic, with the Chancellor responding often to the latest actions or events that have hit the economy hard.

At some stage soon, as he seems to recognise, he needs to put at ease peoples’ and firms’ likely growing anxiety about debt how this will be paid for. Indeed, his necessary actions yesterday have not yet been fully costed.

Just as the last decade has shown that unconventional monetary policy has become the norm, we are now in the space of unconventional fiscal policy. This comes with the unavoidable price of a new crop of zombie firms, staying afloat, servicing debts.

Despite that, it is good to see that the Chancellor has stepped up to the plate. The problem in the UK is not that assistance is being provided in these difficult economic times, it is that when the economy performs well policy tends not to put back on an even keel. In those good times, interest rates rarely go as high as they should and the government does not run budget surpluses. Thus, when policy needs to be eased, as now, it does not always happen from a position of strength.

The UK needs to avoid now the triple policy whammy of a national lockdown, negative interest rates and a tax bombshell. None of these would help. This week our independent Bank of England did not feel constrained about opining on fiscal matters and the need to provide further assistance to those sectors in difficulty. It is a point I have been stressing for some time. But it begs the question as to what else the Bank should be doing to ensure monetary and financial stability and to support the economic agenda?

The economy is recovering but it is at best two-speed. In the wake of continued restrictions, some areas like the creative sector (a massive 5.8% of the economy, although it does cover a broad array of areas) and hospitality sector are in the doldrums and thus the Chancellor was right to provide further assistance. In contrast, areas like retail and construction are recovering relatively solidly. Their pace of rebound may possibly be dampened by the latest restrictions to curb the virus, but it is hard to quantify fully.

The economy still looks set to return to pre-crisis levels by the end of next year. However, there will be a triple legacy.

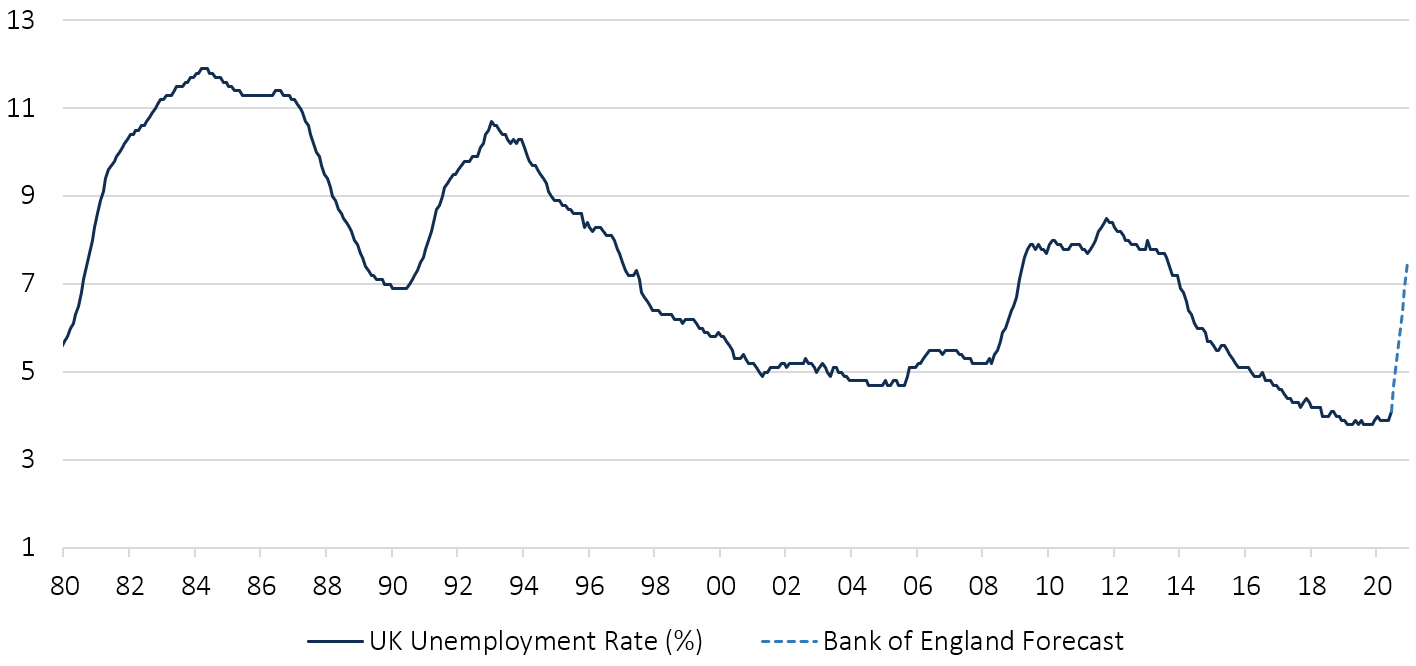

One, is high unemployment. This could absorb much of the policy oxygen of Downing Street. The temptation is to say this will highlight the need for skills and training. That is right but it will be more than that. Increased demand is needed, too, and that was something the Chancellor did not address directly yesterday.

UK Unemployment

Source: Bloomberg, Bank of England, Netwealth calculations

Second, is high private sector debt. Giving firms more time to repay debts helps, but it does not remove the fact that the debt burden will likely restrict the ability of small firms to invest and recruit. Further help to ease this debt burden will likely be needed, including a coronavirus recovery fund.

The third legacy is the public sector debt burden. Budget gaps have to be closed, but not always immediately. There is no magic money tree. Austerity is wrong, but that does not mean a free-for-all on public spending. There is still a need for control. The UK should take advantage of present low yields to issue very long dated Gilts, increasing the already lengthy maturity of our debt, with permanent consols, or bonds perhaps of fifty and one hundred years if the demand exists. One imagines that many global pension funds and insurance firms with long-term liabilities may be welcome buyers.

UK Public Sector Net Debt

Source: Bloomberg

Raising the tax burden is to be avoided although specific hikes, like cuts, will always be there. Instead the focus is about raising the tax base and future tax revenues through stronger economic growth.

This is where we have failed for some time, and it requires a supply-side agenda. That agenda should provide an enabling environment for business, encouraging breakthrough innovation and higher investment helped by infrastructure and incentives.

An immediate challenge is for business, large and small, perhaps encouraged by yesterday’s measures, to try to hold on to as many staff as possible, to not cut internships and apprenticeships and to take on young workers. In this context, it was welcome that the Chancellor continues to provide support. But it also brings us back to what next?

The Prime Minister was right earlier this week to highlight the need to get the balance right between lives and livelihoods. In other words, addressing the health issues linked to the virus but not at the expense of the economy.

Thankfully, a national lockdown was avoided. Such a future option should be ruled out, but clearly it depends upon the health data. It is here that the PM, in my view, needs to provide more of a glimmer of hope to the business world. He indicated not only that the present restrictions will remain in place for six months, but that if they are changed they are more likely to be tightened, not loosened.

Testing, track and trace, plus behaviours are key to keeping the virus in check. While there was an overwhelming case for a lockdown in March, based on the data at the time, the situation appears very different now. Positive tests are rising. This, as the PM outlined, carries with it risks. No-one is denying that. But risks need to be kept in context. In a vaccine gap phase we can’t remove the virus, but can reduce its impact. Even if positive tests rise further, but hospital admissions and deaths stay low, then there is surely a case for the current restrictive measures to be eased – avoiding the need to wait for the six-month timeline.

Moreover, if the evidence from Australia and elsewhere in the southern hemisphere is anything to go by, the imminent flu season may prove weak. Over there, social distancing and other measures to keep the virus in check have seen a weak flu season. If repeated here that, too, would reduce pressure on our health system.

The health data is key, but the case to ease restrictions on business, as soon as it is appropriate to do so, is strong. Even more so when one notes the wider health as well as economic damage caused by restrictions. We need to return the economy to normal, sooner, not later.

Please note, the value of your investments can go down as well as up

This article was written in response to the Chancellor’s Winter Economic Statement that was delivered on 24th September, 2020 and it appeared in the Spectator online on Friday 25th September.